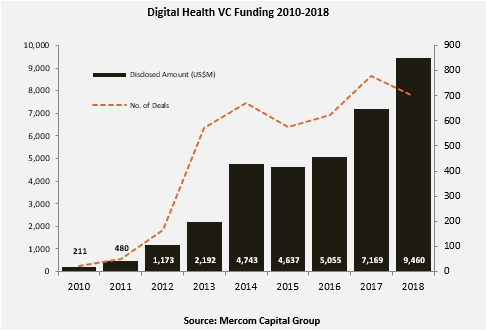

Global venture capital (VC) funding in digital health, including private equity and corporate venture capital, saw another record-breaking year in 2018 with $9.5 billion raised in 698 deals, a 32% increase from the previous record set in 2017 of $7.2 billion in 778 deals. Total corporate funding for Digital Health companies – including debt and public market financing – reached $13 billion in 2018, a 58% increase from the $8.2 billion raised in 2017.

Click here to get the report!

In 2018, announced debt and public market financing for Digital Health companies increased more than three-fold from the previous year with approximately $3.5 billion raised in 21 deals in 2018, compared to $1 billion raised by 34 deals in 2017.

In the United States, digital health companies raised close to $7 billion in 2018 with the remaining $2.5 billion coming out of other countries.

Since 2010, digital health companies have received $35 billion in VC funding in over 4,000 deals and almost $12 billion in debt and public market financing (including IPOs), bringing the cumulative funding total for the sector to $47 billion.

A third of the venture capital funding was raised by just 18 companies, each bringing in over $100 million in 2018.

“Venture capital funding in Digital Health hit another high with almost $10 billion raised. Venture capitalists’ love of digital health companies is evident, but Wall Street is not yet convinced as more than 60 percent of publicly-traded digital health stocks traded below the S&P 500 in 2018,” commented Raj Prabhu, CEO and Co-Founder of Mercom Capital Group. “Funding deals every year have significantly outpaced M&A and IPO activity and exits continue to be a big challenge for digital health companies,” said Prabhu.

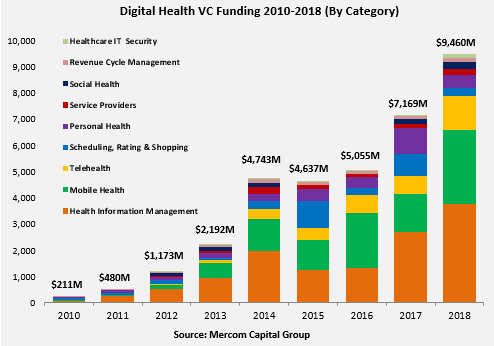

Consumer-centric companies brought in $5.2 billion in 447 deals in 2018, up 24 percent from $4.2 billion raised in 514 deals in 2017. Practice-centric companies raised close to $4.3 billion in 251 deals in 2018, a 43% increase compared to the $3 billion raised in 264 deals in 2017.

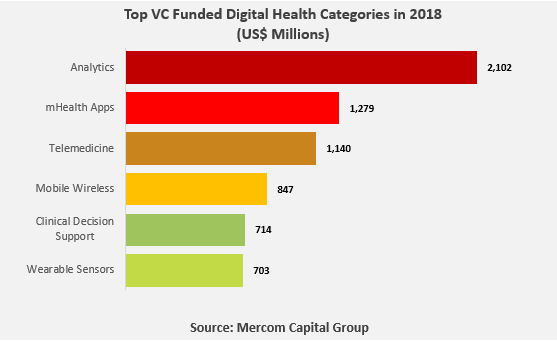

The highest funded categories in 2018 included: Data Analytics with $2.1 billion, mHealth Apps with $1.3 billion, Telemedicine with $1.1 billion, Mobile Wireless Technology companies with $847 million, Clinical Decision Support with $714 million, and Wearable Sensors Technology companies with $703 million.

Categories that witnessed significant year-over-year (YoY) funding growth were: Analytics, mHealth Apps, Telemedicine and Mobile Wireless Technology companies.

Continuing the trend of previous years, Data Analytics remained the top funded category.

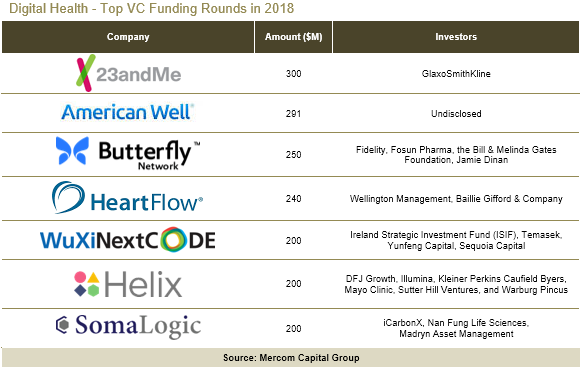

The top VC funding rounds in 2018 included: 23andMe with $300 million, American Well with $291 million, Butterfly Network with $250 million, HeartFlow with $240 million, and WuXi NextCode, Helix, and SomaLogic with $200 million each.

VC participation increased in 2018, with the total number of investors (including accelerators and incubators) rising to 1,396 from 1,288 investors in 2017. The most active VC investors in 2018 were Khosla Ventures, New Enterprise Associates (NEA), and Oak HC/FT.

There were 223 M&A transactions in 2018, compared to the 203 transactions in 2017. There were 18 companies that participated in multiple transactions in 2018.

mHealth Apps were the most acquired category in 2018 with 32, followed by Data Analytics companies with 27 transactions, and companies offering Practice Management Solutions with 22 transactions.

There were 271 companies that made multiple acquisitions from 2010 to 2018. During 2018, Mediware Information Systems and WebMD acquired four companies each while DAS Health, ResMed, Revint Solutions,

Varian, and Virgin Pulse acquired three companies each, and Allscripts, Change Healthcare, Clearlake Capital Group, Inspirata, InTouch Health, Marlin Equity Partners, Netsmart, Philips, Press Ganey Associates, TransUnion, and Waystar (formerly ZirMed) acquired two companies each.

![]()

The top five disclosed M&A transactions in 2018 were: Veritas Capital and Elliott Management’s acquisition of athenahealth for $5.5 billion, Platinum Equity’s acquisition of LifeScan for $2.1 billion, Vista Equity Partners’ acquisition of MINDBODY for $1.9 billion, Roche’s acquisition of Flatiron Health for $1.9 billion, Inovalon’s acquisition of ABILITY Network for $1.2 billion, Veritas Capital’s acquisition of General Electric’s (GE) Healthcare IT division for $1 billion, and 3M’s acquisition of M*Modal for $1 billion.

![]()

To learn more about the report, visit: https://mercomcapital.com/product/2018-q4-annual-healthcare-digital-health-funding-ma-report/

Image credit: Ergo Group