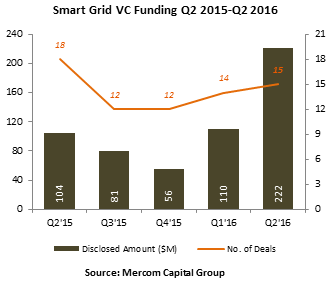

Venture capital (VC) funding (including private equity and corporate venture capital) for Smart Grid companies doubled with $222 million in 15 deals compared to $110 million in 14 deals in Q1 2016. Year-over-year (YoY), funding also doubled compared to Q2 2015 when $104 million was raised in 18 deals.

To get a copy of the report, visit: https://mercomcapital.com/product/q2-2016-smart-grid-batterystorage-efficiency-funding-ma-report/

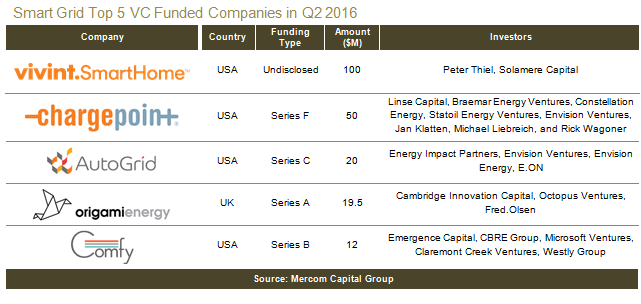

The top VC funded Smart Grid related technology companies included Vivint Smart Home, which raised $100 million from tech investor Peter Thiel and investment firm Solamere Capital; ChargePoint, which raised $50 million from Linse Capital, Braemar Energy Ventures, Constellation Energy, Statoil Energy Ventures, Envision Ventures, Jan Klatten, Michael Liebreich, and Rick Wagoner; AutoGrid Systems, which raised $20 million from a consortium of global investors including Energy Impact Partners, Envision Ventures, Envision Energy and E.ON; Origami Energy, which brought in $19.5 million from Cambridge Innovation Capital, Octopus Ventures, and Fred Olsen-related companies; and lastly Comfy secured $12 million in funding from Emergence Capital, CBRE Group, Microsoft Ventures, Claremont Creek Ventures, and Westly Group.

The top VC funded Smart Grid related technology companies included Vivint Smart Home, which raised $100 million from tech investor Peter Thiel and investment firm Solamere Capital; ChargePoint, which raised $50 million from Linse Capital, Braemar Energy Ventures, Constellation Energy, Statoil Energy Ventures, Envision Ventures, Jan Klatten, Michael Liebreich, and Rick Wagoner; AutoGrid Systems, which raised $20 million from a consortium of global investors including Energy Impact Partners, Envision Ventures, Envision Energy and E.ON; Origami Energy, which brought in $19.5 million from Cambridge Innovation Capital, Octopus Ventures, and Fred Olsen-related companies; and lastly Comfy secured $12 million in funding from Emergence Capital, CBRE Group, Microsoft Ventures, Claremont Creek Ventures, and Westly Group.

There were 46 VC investors that participated in Smart Grid deals in Q2 2016 compared to 22 in Q1 2016. Smart Grid Communication technologies, including Home Automation, had the largest share of VC funding with $123 million, a substantial increase from the $31 million raised in four deals in Q1 2016.

There was one debt financing deal announced in the second quarter of 2016 for $3 million, compared to $214 million in two debt & public market financing deals in the previous quarter.

There were three M&A transactions for Smart Grid technologies in Q2 2016 (one disclosed) compared to two transactions (one disclosed) in Q1 2016.

Battery/Storage

VC funding for Battery/Storage companies doubled with $125 million in 10 deals in Q2 2016 compared to $54 million in 10 deals in the previous quarter. Year-over-year funding in Q2 2016 was in line with Q2 2015, which had $126 million in 13 deals.

VC funding in Q2 2016 was spread across six Battery/Storage sub-technologies: lithium-ion batteries, sodium-based batteries, energy storage systems, lead-based batteries, energy storage management software and thermal energy storage.

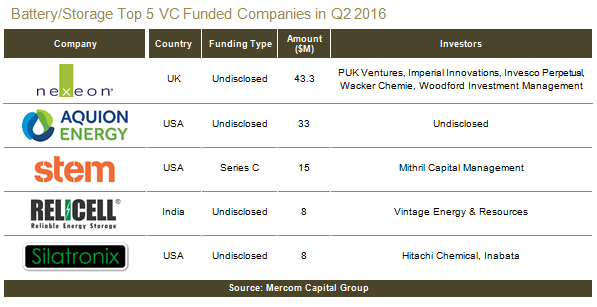

The Top 5 Battery/Storage VC funding deals were: Nexeon with $43.3 million from PUK Ventures, Imperial Innovations, Invesco Perpetual, Wacker Chemie and Woodford Investment Management; Aquion Energy with $33 million; Stem with $15 million from Mithril Capital Management, Greenvision Technologies (brand name Relicell) with $8 million from Vintage Energy & Resources; and Silatronix with $8 million from Hitachi Chemical and Inabata.

Twenty investors participated in Battery and Storage funding in Q2 2016 compared to eight in Q1 2016. Lithium-ion Battery companies raised the most funding with $51.3 million in three deals.

Announced debt and public market financing for Battery/Storage technologies came to $65 million in two deals in the second quarter of 2016, compared to $28.5 million in two deals in Q1 2016. Plug Power and FuelCell Energy closed on a long-term loan facility for $40 million and $25 million respectively with Hercules Capital.

There were four M&A transactions for Battery/Storage companies in Q2 2016 two of which disclosed financial details. In Q1 2016, there were two M&A transactions, neither disclosed transaction details. The largest M&A deal in the second quarter of 2016 was the $1.1 billion acquisition of Saft by Total.

Efficiency

There was a sharp decline in VC funding for Energy Efficiency technology companies in Q2 2016 with $86 million in nine deals compared to $211 million in 14 deals in Q1 2016. In a YoY comparison, VC funding for Efficiency companies in Q2 2015 was $211 million with twice as many deals with 18.

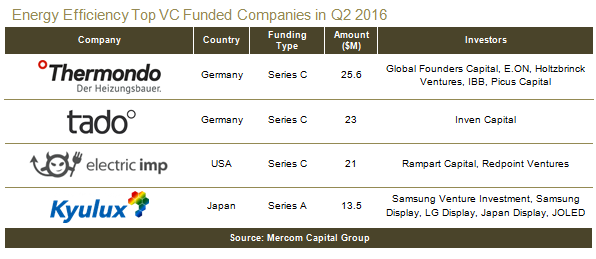

The top VC funded company in Q2 2016 was Thermondo which raised over $25.6 million in funding from: Global Founders Capital, E.ON, Holtzbrinck Ventures, IBB, and Picus Capital, followed by tado° which raised $23 million in funding from Inven Capital, Electric Imp which raised $21 million in funding from Rampart Capital and Redpoint Ventures and Kyulux which raised $13.5 million from Samsung Venture Investment, Samsung Display, LG Display, Japan Display, JOLED, top tier Japanese venture capital funds and a Japanese government affiliated venture fund.

Eighteen investors participated in Energy Efficiency VC deals in Q2 2016 compared to 31 in the previous quarter.

Announced debt and public market financing in the Efficiency category peaked in the second quarter of 2016 with $1.75 billion in seven deals. In Q1 2016 there were two debt deals for $238 million.

There was one initial public offering (IPO) in the Efficiency category by Philips Lighting, which accounted for $959 million.

In Q2 PACE Financing totaled $762 million including $512 million in PACE Securitization deals from three transactions. Top deals included the $305.3 million raised by Renovate America, through its seventh securitization of PACE bonds; $250 million credit facility secured by Ygrene Energy Fund to support the expansion of its PACE program investments and $123 million raised by Renew Financial through its second securitization of residential PACE bonds.

M&A transactions in the Efficiency sector doubled in the second quarter of 2016 with seven transactions (three disclosed) compared to three transactions in Q1 2016 of which only one disclosed details. The top deal was the $532 million acquisition of Opower by Oracle. Another notable deal was the merger of Dividend Solar and Figtree Financing.

Image credit “Energy Storage System” (CC BY-ND 2.0) by portland general