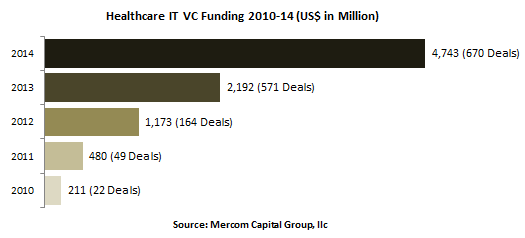

Venture capital (VC) funding in the Health IT sector more than doubled in 2014, coming in at $4.7 billion in 670 deals compared to $2.2 billion in 571 deals in 2013. The sector also brought in $2.1 billion in debt and public market financing including six IPOs, bringing the total corporate funding raised in the sector in 2014 to almost $7 billion.

VC funding increased in Q4 2014 with $1.2 billion in 134 deals compared to $956 million in 212 deals in Q3 2014.

To get a copy of this report, please email us at info@mercomcapital.com

“The Digital Health sector had another phenomenal fundraising year. In the five years since we started tracking funding data, the sector has raised $8.8 billion in VC funding and another $3.6 billion in public market and debt financings bringing the total to $12.4 billion – largely driven by the HITECH and Affordable Care Act. However, the enthusiasm in the sector shown by the VC community was not quite matched by the public markets when you look at market performance of companies that went the IPO route in 2014,” commented Raj Prabhu, CEO and Co-Founder of Mercom Capital Group.

“The Digital Health sector had another phenomenal fundraising year. In the five years since we started tracking funding data, the sector has raised $8.8 billion in VC funding and another $3.6 billion in public market and debt financings bringing the total to $12.4 billion – largely driven by the HITECH and Affordable Care Act. However, the enthusiasm in the sector shown by the VC community was not quite matched by the public markets when you look at market performance of companies that went the IPO route in 2014,” commented Raj Prabhu, CEO and Co-Founder of Mercom Capital Group.

Practice-centric companies raised $2.4 billion in 234 deals in 2014, including Clinical Decision Support companies with $517 million, followed by Data Analytics companies with $367 million and Population Health Management companies with $247 million.

Consumer-centric companies raised $2.3 billion in 436 deals. Mobile Health (mHealth) companies were the largest recipient of VC funding bringing in $1.2 billion – within mHealth most funding went to Wearables with $526M and mHealth Apps with $507M. Telehealth companies received $369 million, Rating and Comparison Shopping companies brought in $288 million.

Notable technology areas with significant YoY growth:

mHealth apps: 341%

Telehealth: 297%

Rating and comparison shopping: 216%

Data analytics: 146%

Wearables: 136%

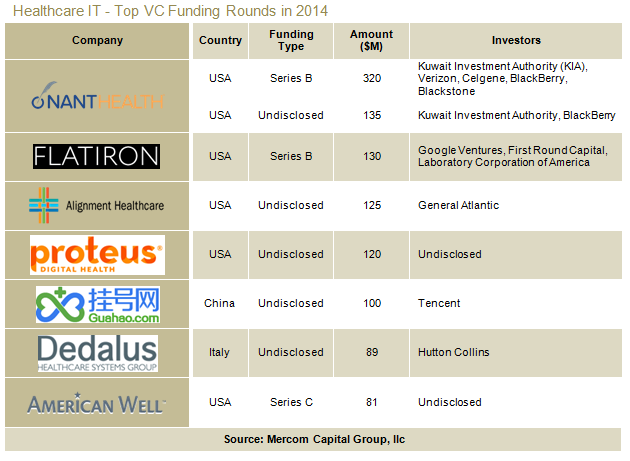

The top two VC funding rounds in 2014 were raised by NantHealth which brought in $320 million and $135 million in two separate deals; Flatiron Health raised $130 million; this was followed by Alignment Healthcare which raised $125 million. Proteus Digital Health came in next with its $120 million raise (they also raised $52 million in another deal bringing its total to $172 million for 2014); China’s Guahao.com raised $100 million; Dedalus Group raised $89 million; and American Well brought in $81 million.

A total of 732 investors were involved in funding rounds for Healthcare IT companies in 2014. The top VC investors were Khosla Ventures and The Social+Capital Partnership with nine deals each, followed by Kleiner Perkins Caufield & Byers and Sequoia Capital with seven deals each.

Top investors in the sector from the past five years were Khosla Ventures with 21 deals, The Social+Capital Partnership with 18, Kleiner Perkins Caufield & Byers with 17, Sequoia Capital with 12 and Andreessen Horowitz with 10 deals.

There were 120 accelerator and incubator deals in 2014 compared to 139 in 2013. Top accelerator/incubator seed investors were Blueprint Health, Rock Health, Y Combinator, DreamIt Ventures, Sprint Accelerator, The Iron Yard and XLerate Health.

A record 29 countries participated in Health IT VC funding activity this year. In the United States, California led Digital Health fundraising with 174 deals followed by New York with 50, Massachusetts with 33, Florida with 22, and Texas with 21.

There were 219 M&A transactions in the Health IT sector in 2014 compared to 165 transactions in 2013, with 21 companies making multiple transactions during the year.

“Most of the M&A activity has been around larger, more established practice-focused companies. Even though Mobile Health related apps and wearables are getting significant funding, we have not seen a game-changing Instagram or WhatsApp-type transaction yet in the sector,” continued Prabhu.

Revenue Cycle Management companies led M&A activity with 28 transactions followed by Practice Management with 24 and Mobile Health with 21.

In the last five years, 121 companies have made multiple acquisitions including IMS Health with eight, CompuGroup Medical, Emdeon, iMedx and Quality Systems with seven each, and both McKesson and PracticeMax with six companies apiece. Cerner, GE Healthcare, Nuance Communications and The Advisory Board Company each acquired five companies.

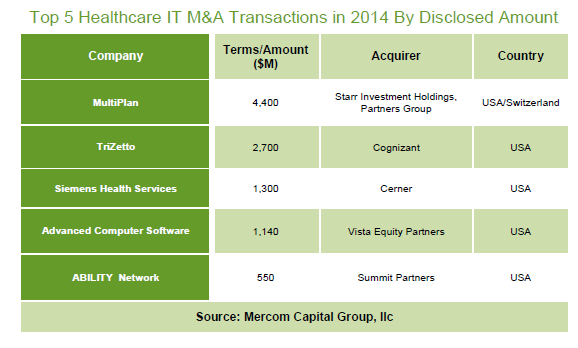

The Top 5 disclosed M&A transactions included the $4.4 billion acquisition of MultiPlan by Starr Investment Holdings and Partners Group, the acquisition of TriZetto by Cognizant for $2.7 billion, and the $1.3 billion acquisition of Siemens’ health information technology business unit, Siemens Health Services, by Cerner. This was followed by Vista Equity Partners’ acquisition of Advanced Computer Software for $1.14 billion, and the $550 million acquisition of ABILITY Network by Summit Partners.

There were six Digital Health IPOs in 2014, raising a total of $1.8 billion. IMS Health raised $1.3 billion, followed by Castlight Health with $204 million, Everyday Health with $100 million, Orion Health with $98 million, Imprivata with $86 million and Connecture with $53 million.

There were six Digital Health IPOs in 2014, raising a total of $1.8 billion. IMS Health raised $1.3 billion, followed by Castlight Health with $204 million, Everyday Health with $100 million, Orion Health with $98 million, Imprivata with $86 million and Connecture with $53 million.

To get a copy of this report, please email us at info@mercomcapital.com