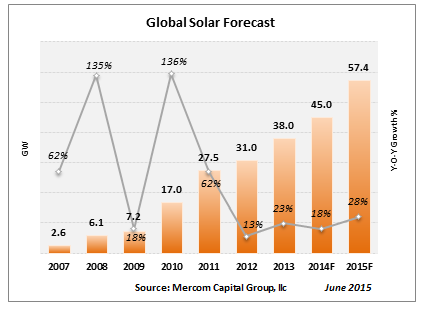

Mercom Capital Group, llc, a global clean energy communications and consulting firm, projects a strong year for solar, forecasting global installations to reach 57.4 GW in 2015.

“We are revising our forecast upwards since our previous update due to positive news coming out of China along with revised installation goals,” said Raj Prabhu, CEO and Co-Founder of Mercom Capital Group.

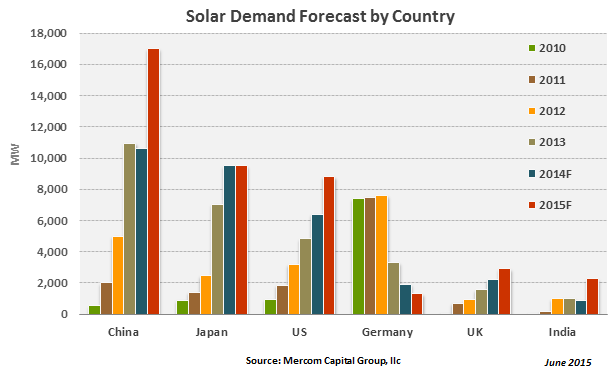

Mercom expects China, Japan and the U.S. to account for approximately 60 percent of global solar installations this year. Since Mercom’s previous forecast three months ago, China has revised its solar installation target yet again by 20 percent to almost 18 GW for 2015. “With the specific steps put forward by the National Energy Administration (NEA) and the 5 GW already installed in the first quarter, 17.8 GW is a more achievable target this year. Omission of a specific installation target for distributed solar projects, which contributed to missing the 2014 goal, is a positive,” further commented Prabhu. China’s solar installation goals were revised numerous times last year, and a similar trend can be expected this year if there are implementation issues on the ground.

Trade skirmishes are now a familiar part of the solar sector. The European Union (EU) announced that it has opened investigations into imports from Taiwan and Malaysia. The EU is following the US-China template where antidumping duties were imposed on Chinese manufacturers, followed by another case against circumvention. The EU recently imposed tariffs on three solar companies for violating the minimum tariff agreement between China and the EU. The EU is also reviewing the current minimum import price agreement which is due to expire in December of this year.

Mercom forecasts Japanese solar installations in 2015 to be approximately 10 GW. The Ministry of Economy, Trade and Commerce (METI) announced feed-in tariff (FiT) cuts in March.

Solar PV installations in Germany continue on a downward trend with only 400 MW installed in the first four months of 2015 compared to 622 MW installed during the same time last year. Germany’s forecast has been reduced to 1,300 MW for 2015.

The first auction for large-scale PV projects in Germany was announced in April for 150 MW and was oversubscribed by four times. Under auction rules the lowest bid wins. The auction was implemented as a cheaper alternative to the FiT, but turned out to be a slightly more expensive option. The second auction is scheduled for August and if this trend persists, there is a good chance the program will be modified after this year.

The U.S. is expected to install approximately 8.8 GW of solar in 2015 as projects ramp up to beat the December 31, 2016 federal Investment Tax Credit (ITC) expiration; 2015 and 2016 are forecasted to be its two best years prior to the impending deadline.

The U.S. market has been the leader in reducing financing costs by using innovative financing structures like securitization and Yieldcos. In the first half of this year, third-party solar finance companies have raised almost $3 billion dollars in lease and loan funds, on course to make this the best fundraising year for solar lease companies. As the ITC expiration draws closer, we expect this activity to strengthen in 2016.

The U.K. is expected to have its best year for solar installations in 2015 with an expected rush before the April 2015 expiration of Renewables Obligation Certificates (ROC) for projects larger than 5 MW. The market going forward is expected to move towards smaller projects that are incentivized through the FiT program.

Mercom has revised its solar demand forecast for India to about 2.2 GW. Click here for complete India update http://bit.ly/mercomsfo2.

Subscribers to Mercom’s weekly Solar Market Intelligence Report will have access to the full update. To become a subscriber, visit: https://mercomcapital.com/subscribe.

Image credit: First Solar