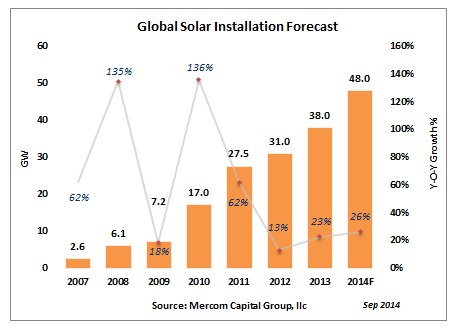

The first half of 2014 was not spectacular for solar installations globally, but with recent policy adjustments being implemented, especially in China, another strong year is forecasted with installations of approximately 48 GW in total, according to the latest quarterly update from Mercom Capital Group, llc, a global clean energy communications and consulting firm.

Raj Prabhu, CEO and Co-Founder of Mercom Capital Group, commented that “After a slow first half, it will be a rush to the finish for global solar installations this year with a lot depending on execution in China, Japan and the UK”.

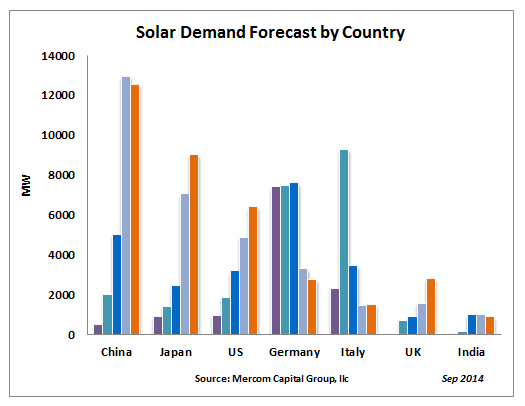

China did not perform strongly in the first half, installing just 3.3 GW, but this prompted recent policy changes with strong support for distributed generation (DG). China also reduced its 2014 installation target from 14 GW to 13 GW. Though reaching this goal may prove challenging (we said the same last year and installations overshot the target) this year, policy foundation has been laid for a strong few years to come. As we mentioned in our prior update, China’s 8 GW target previously set for DG was aggressive and unachievable. With the change of definition of a DG project to any project upto 20 MW, it will become a lot easier to achieve the target.

Japan, with its attractive feed-in tariff (FiT) and energy shortage scenario, is a growing market for solar, and has a large pipeline of projects. METI has been auditing the project pipeline and cancelling projects that have not made any progress. According to the new rules applicable from April 1 this year, solar developers are required to secure land and equipment within six months of getting approvals to avoid their projects being cancelled, which will clean up the project pipeline. The current Abe administration in Japan continues to work towards bringing nuclear energy back online slowly as the trade deficit has ballooned due to liquefied natural gas (LNG) imports. This will not be easy as the majority of the population is still opposed to the reintroduction of nuclear energy.

The Indian solar market has been stuck around the 1 GW mark for the last few years. With a new administration in power, policy makers have gone back to the drawing board and are in the process of implementing new programs which will have much bigger installation targets. All signs point to the Indian solar market taking off after 2015 and it could become one of the larger markets along with China, Japan, and the United States.

The U.S. solar market has been advancing strongly in spite of trade disputes with China, Taiwan and India and without a central policy like in China, Japan or Germany. The US Department of Commerce announced preliminary antidumping duties on China and Taiwan in an attempt to close a loophole for Chinese manufacturers.

“Though there aren’t any strong signs that this is adversely affecting the markets, the time has come to settle these disputes,” commented Prabhu.

While the United States lags behind Germany in installation costs, it has been at the forefront in developing innovative financing structures to bring the cost of capital down. Solar leases and securitization are examples of such structures that are now being implemented worldwide. The last quarter saw a number of announcements about Yieldcos. Financing structures continue to evolve as the market prepares for the expiration of the investment tax credit (ITC) in 2016.

The UK solar market continues to defy expectations and has become the most important PV market in Europe after Germany, and could possibly overtake Germany in installations in 2014. UK installations are set to more than double if this year’s installation pace continues through Q3 and Q4. The rush before the expiration of the Renewables Obligation in April 2015 will likely drive installations towards the end of the year.

PV installations in Germany have continued to slow down after a record 56 percent drop in 2013. Installations through July this year were at 1.4 GW, July being the best month for installations with 345 MW ahead of the Renewable Energy Sources Act (EEG) 2014 (which took effect from August 1, 2014). The year should end with installations in the 2.5-3 GW range.

Subscribers to Mercom’s weekly Solar Market Intelligence Report will have access to the full update. To become a subscriber, visit: https://mercomcapital.com/subscribe.