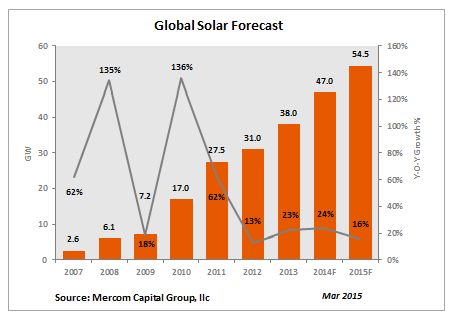

The solar industry is forecasted to continue its growth in 2015 with installations reaching approximately 54.5 GW according to the latest quarterly update from Mercom Capital Group, llc, a global clean energy communications and consulting firm.

“China and Japan have to overcome some implementation issues for 2015 to be another good year for global solar installations,” said Raj Prabhu, CEO and Co-Founder of Mercom Capital Group. “On the positive side, new funding mechanisms are helping reduce the cost of financing and are bringing in new streams of funding into the sector.”

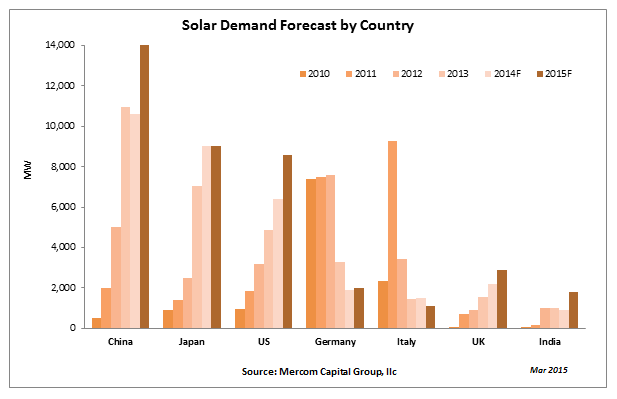

While actual installation numbers for 2014 are trickling in, China recently reported installation figures of 10.60 GW which implies that it missed its installation goal of 13 GW by more than 2 GW. This will have implications on total global installations. China also revised its 2013 actual installation figures down from 12.9 GW to 10.95 GW. NEA’s latest target is a very aggressive 17.8 GW for 2015. Japan is forecasted to have installed approximately 9 GW in 2014 and is expected to be in a similar range for 2015. Japan’s Ministry of Economy, Trade and Commerce (METI) just announced the revised FiT for FY 2015. The revised tariff is lowered by approximately 16 percent for projects >10kW. Mercom is forecasting Japanese installations to peak in 2015.

The U.S. solar market is forecasted to grow at a rapid pace in 2015 and reach more than 8.5 GW as installations accelerate with the looming ITC expiration deadline at the end of next year. 2016 will undoubtedly be a big year for solar due to the expected installation rush before the ITC expiration, but the push for installations has already begun.

U.S. trade disputes with China remain a thorn for the solar sector in 2015.

The European solar market continues to shrink with Germany installing only 1.9 GW in 2014 (its lowest installation total in five years). Installation levels are forecasted to be similar in 2015 primarily due to the decline in incentives.

The U.K. was the most active European market with 2.2 GW installed in 2014 and 2.9 GW forecasted in 2015. The U.K. solar market in 2014 was largely driven by Renewables Obligation Certificates (ROC) for projects larger than 5 MW. This will likely be the best year for solar in the U.K., and decline thereafter.

Indian solar installations in calendar year 2014 totaled 883 MW, down slightly compared to 1,004 MW installed in 2013. India failed to reach the GW mark in 2014 but is expected to double in size to about 1.8 GW in 2015.

Overall, we are predicting another solid year for the global solar industry.

Subscribers to Mercom’s weekly Solar Market Intelligence Report will have access to the full update. To become a subscriber, visit: https://mercomcapital.com/subscribe.

Image credit: Nuvest Management Services