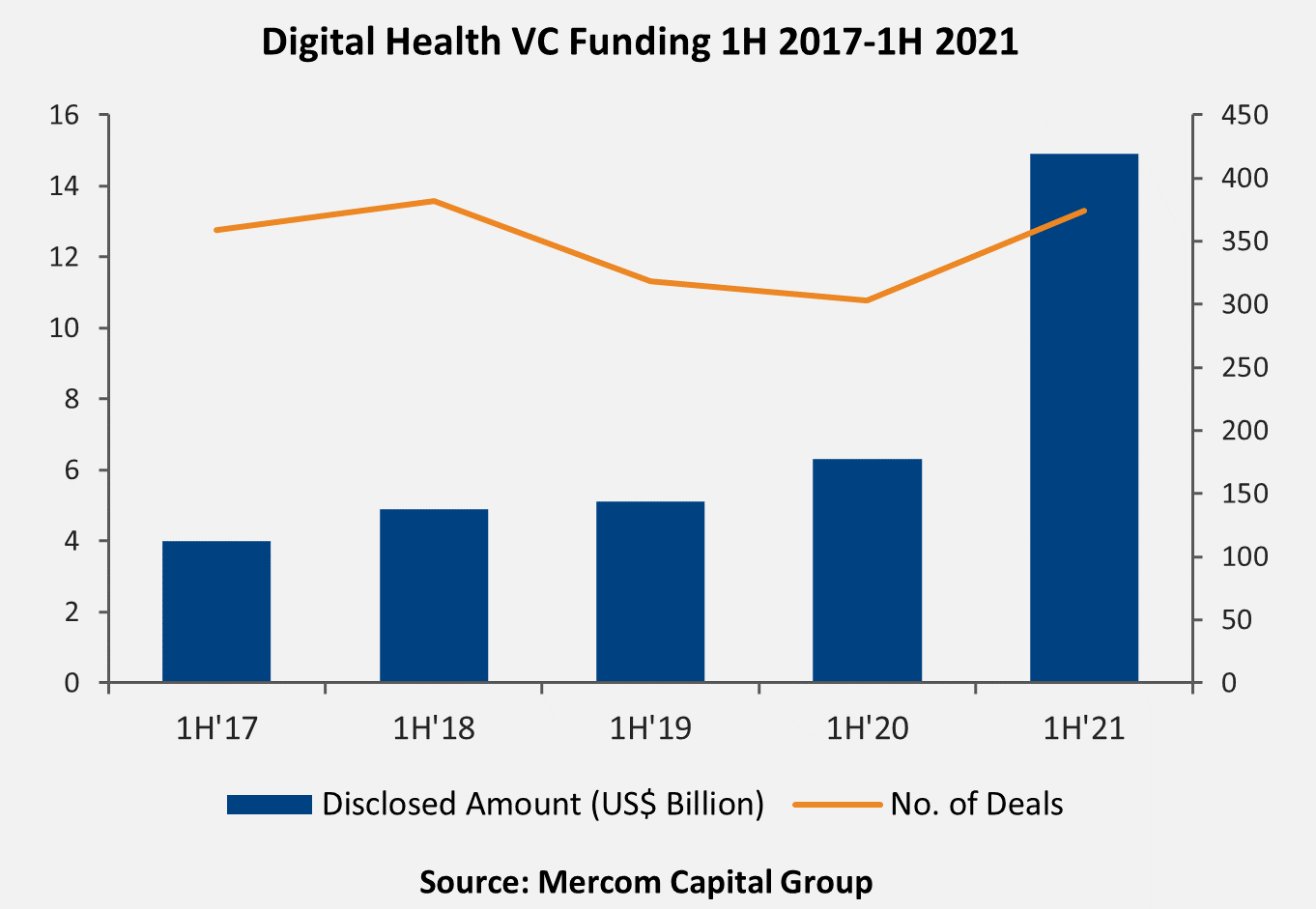

Global VC funding for Digital Health companies in the first half (1H) of 2021 shattered all previous 1H funding records, with $15 billion. Funding activity was up by 138% during 1H 2021, compared to $6.3 billion raised in 1H 2020.

To learn more about the report and download a free executive summary, visit:

https://mercomcapital.com/product/1h-q2-2021-digital-health-healthcare-it-funding-ma-report

Corporate funding into digital health companies, including VC, public market financing, and debt totaled $19 billion in 1H 2021.

In Q2 2021, Digital Health companies raised a record $7.7 billion in 195 deals, a 7% increase quarter-over-quarter (QoQ) compared to $7.2 billion raised in 179 deals in Q1 2021. Year-over-year (YoY) funding was up by 175% compared to $2.8 billion in 161 deals in Q2 2020.

Fifty digital health companies raised $100 million or more in 1H 2021.

“The digital health sector had a spectacular first half of 2021. Venture investments in digital health during 1H 2021 have already surpassed funding raised in all of 2020 and is the largest amount raised in a single year since 2010. Telehealth again led funding activity, accounting for almost 30% of the funding raised in 1H 2021. An even more impressive data point in the first half of the year was the record M&A activity, which has been flat in previous quarters despite the funding surge. A record 12 companies went public during the first six months of the year,” said Raj Prabhu, CEO of Mercom Capital Group.

Digital Health consumer-centric companies accounted for 69% of the funding in Q2 2021, raising $5.3 billion in 129 deals, while practice-centric companies accounted for 31%, raising $2.4 billion in 66 deals.

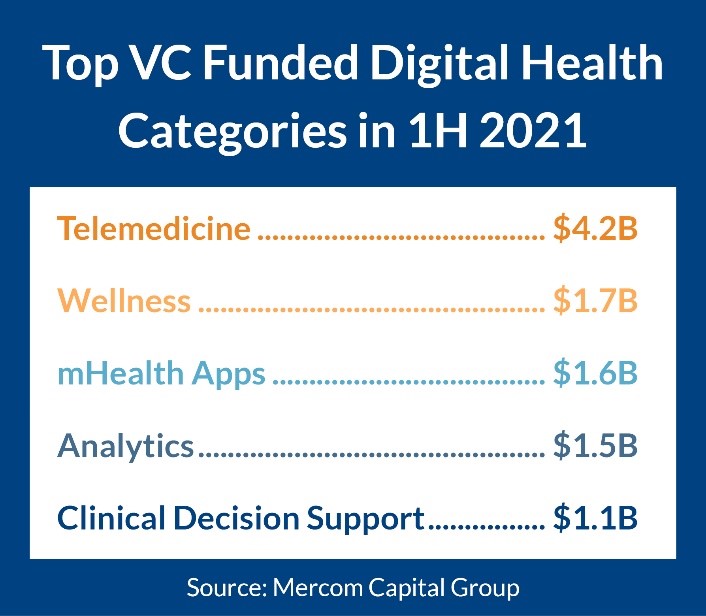

The top-funded Digital Health VC funded categories in 1H 2021 were: Telemedicine with $4.2 billion, Wellness with $1.7 billion, mHealth Apps with $1.6 billion, Analytics with $1.5 billion, and Clinical Decision Support with $1.1 billion.

Telemedicine companies raised $4.2 billion in 105 deals in 1H 2021, a 147% increase in YoY compared to $1.7 billion raised in 79 deals in 1H 2020.

Top categories that received funding in Q2 2021 included Telemedicine with $2.2 billion, Wellness with $1.1 billion, mHealth Apps with $667 million, Analytics with $565 million, Practice Management Solutions with $480 million, and Clinical Decision Support with $434 million.

Early round venture capital funding (Seed, Series A) came to $1.6 billion in 1H 2021. Most of the VC funding in early rounds went into Telemedicine, mHealth Apps, and Data Analytics companies.

Seven hundred and seven (707) investors participated in funding deals in Q2 2021 compared to 547 investors in Q1 2021. General Catalyst led Digital Health financing activity during Q2 2021 with 11 funding rounds. Oak HC/FT and Optum Ventures each made six investments, and another 100 investors made two or more investments during Q2 2021.

A record 1,254 investors participated in 1H 2021, compared to 921 investors in 1H 2020.

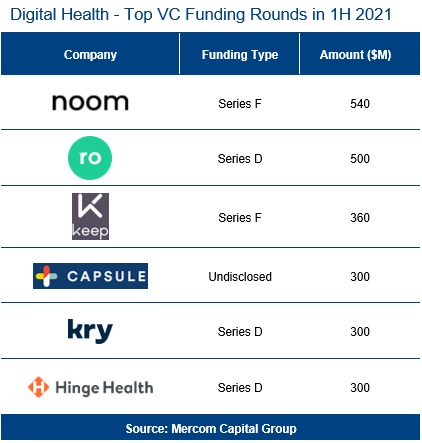

The Top VC deals in 1H 2021 included $540 million raised by Noom, $500 million raised by Roman, $360 million raised by Keep, and $300 million each raised by Capsule, KRY, and Hinge Health.

Twenty-one different countries recorded Digital Health VC funding deals in Q2 2021. Companies in the United States recorded the most VC funding deals with 148.

Sixteen (16) Digital Health products received FDA/CE approvals in Q2 2021 and 279 since Q1 2017.

In 1H 2021, a total of 136 Digital Health M&A transactions were announced compared to 83 in 1H 2020. This is the highest number of M&A transactions recorded in the first half of any year. In Q2 2021, there were 73 M&A transactions compared to 63 M&A transactions in Q1 2021.

Telemedicine companies led M&A activity in 1H 2021 with 25 transactions, followed by Practice Management Solutions companies with 20 transactions. Analytics, Clinical Decision Support, and mHealth Apps each recorded 10 M&A transactions during 1H 2021.

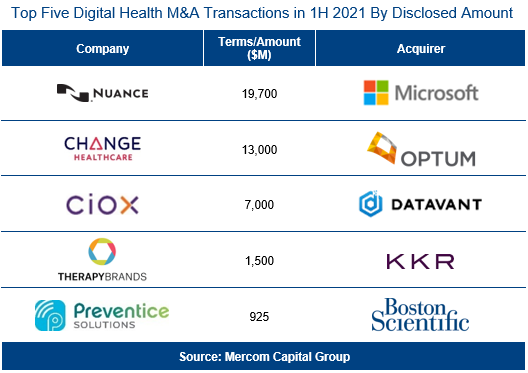

Notable M&A transactions in 1H 2021 were: Microsoft’s acquisition of Nuance for $19.7 billion, Optum’s acquisition of Change Healthcare for $13 billion, Datavant’s acquisition of Ciox Health for $7 billion, KKR’s acquisition of Therapy Brands for $1.5 billion, and Boston Scientific’s acquisition of Preventice Solutions for $925 million.

This report is 126 pages in length, contains 70 charts, graphs, and tables, and covers 1,052 investors and companies.