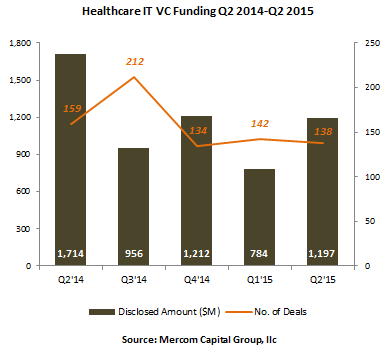

Venture capital (VC) funding, including private equity and corporate venture capital, in the Health IT / Digital Health sector increased 53 percent QoQ, coming in at $1.2 billion in 138 deals compared to $784 million in 142 deals in Q1 2015, but was down nearly 30 percent compared to the same quarter of last year. Debt and public market financing in the sector rose to $1.6 billion in eight deals including four IPOs, bringing the total corporate funding raised in the sector for Q2 2015 to $2.8 billion.

To learn more about the report, visit: https://mercom.wpengine.com/product/q2-2015-healthcare-it-digital-health-funding-and-ma-report/

VC funding has reached almost $2 billion in the first half of 2015 compared to $2.6 billion during the same period in 2014.

“In the Healthcare IT sector, companies raised more money through IPOs than venture capital this quarter,” commented Raj Prabhu, CEO and Co-Founder of Mercom Capital Group. “Growth in public market financing is an encouraging sign for companies in this sector as it opens up another avenue for funding and an exit path for investors. That said, out of 14 IPOs since 2012, six have decreased in value over their IPO price as of the end of last quarter.”

Healthcare practice-centric companies raised $473 million in 41 deals compared to $347 million in 44 deals in Q1 2015. The areas that received the most funding under this category were Clinical Decision Support companies with $206 million, followed by Data Analytics companies with $91 million, Electronic Health Record (EHR) companies with $26 million and Practice Management Solutions companies with $20 million.

Consumer-centric companies raised $724 million in 97 deals this quarter compared to $437 million in 98 deals in Q1 2015. Mobile Health companies brought in $214 million in 37 deals compared to $282 million in 56 deals last quarter, with mHealth Apps receiving $106 million, compared to the $220 million raised in Q1 2015. Personal Health/Wellness companies raised $209 million in 20 deals followed by Telehealth companies which raised $152 million in 18 deals. Rating & Comparison Shopping companies raised $149 million in 20 deals.

“This quarter Telehealth, Personal Health/Wellness, and Rating and Comparison Shopping companies all had their best fundraising quarter, while funding into Mobile Health and Apps dropped,” further commented Prabhu.

There were 39 early-stage deals under $2 million, including six accelerator/incubator deals. Accelerator deals have continued to slow down over the last three quarters.

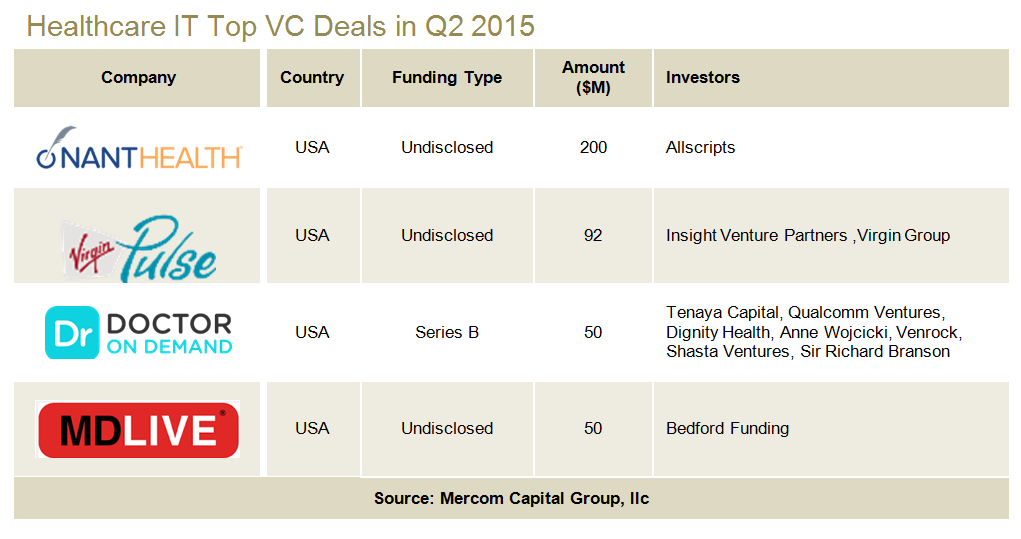

Top VC funding deals in Q2 2015 were the $200 million raised by NantHealth, a cloud-based healthcare IT company delivering care through a single integrated clinical platform; the $92 million raised by Virgin Pulse, a developer of an online employee wellness and engagement platform; the $50 million each secured by Doctor on Demand, a telemedicine platform that enables video consultation with a licensed U.S. physician via mobile apps, and MDLIVE, a provider of virtual telehealth consultations with U.S. board-certified physicians and licensed therapists through a HIPAA-compliant cloud-based platform.

A total of 271 investors including two accelerators/incubators participated in Healthcare IT deals this quarter, 29 of which participated in multiple rounds. The investors with the highest number of funding deals this quarter included Venrock with five, followed by 500 Startups, Cambia Health Solutions, Khosla Ventures, Qualcomm Ventures, Rock Health, Slow Ventures and Tencent Holdings with three each.

A total of 271 investors including two accelerators/incubators participated in Healthcare IT deals this quarter, 29 of which participated in multiple rounds. The investors with the highest number of funding deals this quarter included Venrock with five, followed by 500 Startups, Cambia Health Solutions, Khosla Ventures, Qualcomm Ventures, Rock Health, Slow Ventures and Tencent Holdings with three each.

Globally, U.S. companies raised greater than $1 billion in 111 deals. Fourteen other countries: Canada, Chile, China, Finland, Germany, India, Indonesia, Israel, the Netherlands, Poland, Singapore, Sweden, Switzerland and the UK recorded deals this quarter. In the United States, 37 deals came out of California, followed by New York which recorded 13 deals, Massachusetts with 11 deals and Florida with six deals.

Announced debt and public market financing in Health IT rose to $1.6 billion in eight deals this quarter compared to $975 million in seven deals in Q1 2015. There were four IPOs which together accounted for $1.4 billion. There were a number of large IPOs in the second quarter, led by wearable device maker Fitbit’s $841.2 million offering; Press Ganey Associates, a provider of patient satisfaction surveys and advisory services to health care providers, raised $256 million; Evolent Health, a population health management company, raised $225 million and MINDBODY, a provider of scheduling and business management software for health and wellness companies, raised $100.1 million.

There were 53 M&A transactions (eight disclosed) in the Health IT sector this quarter compared to 56 transactions (14 disclosed) in Q1 2015. Practice-focused companies accounted for the greatest number of M&A transactions with 43 of the 53, while consumer-centric companies had 10 transactions. Twenty-seven HIM companies were acquired this quarter followed by nine Service Providers, six Revenue Cycle Management companies and four Telehealth companies.

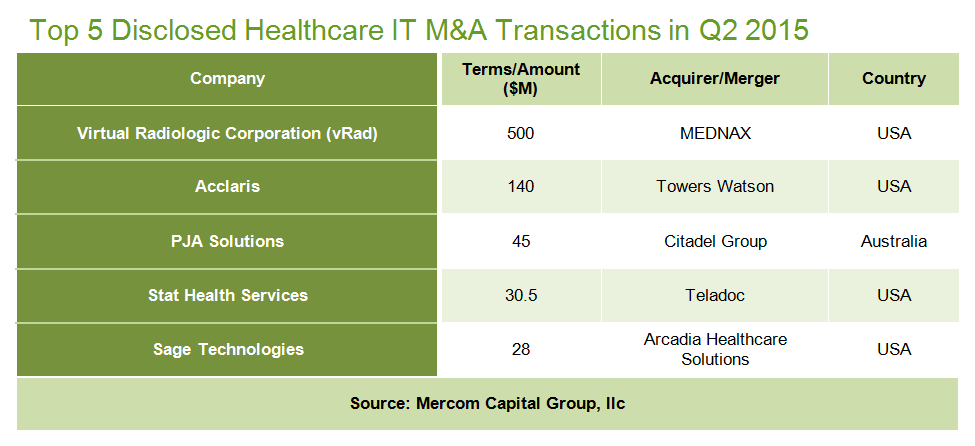

The largest disclosed M&A transaction was the $500 million acquisition of Virtual Radiologic Corporation (vRad), a provider of teleradiology and telemedicine services, by MEDNAX. This was followed by the $140 million acquisition of Acclaris, a provider of SaaS-based technology and services for consumer-driven health care and reimbursement accounts, by Towers Watson.

The Citadel Group acquired PJA Solutions, a provider of laboratory information systems software products for diagnostic laboratories and clinical applications in public hospitals and related sectors, for $45 million. Teladoc acquired Stat Health Services, a provider of telemedicine services for non-emergency health conditions, for $30.5 million and Arcadia Healthcare Solutions acquired Sage Technologies, a provider of management and analytics software for managed-care businesses and accountable care organizations, for $28 million.

The Citadel Group acquired PJA Solutions, a provider of laboratory information systems software products for diagnostic laboratories and clinical applications in public hospitals and related sectors, for $45 million. Teladoc acquired Stat Health Services, a provider of telemedicine services for non-emergency health conditions, for $30.5 million and Arcadia Healthcare Solutions acquired Sage Technologies, a provider of management and analytics software for managed-care businesses and accountable care organizations, for $28 million.

There were a total of 516 companies and investors covered in this comprehensive report.

To learn more about the report, visit: https://mercom.wpengine.com/product/q2-2015-healthcare-it-digital-health-funding-and-ma-report/