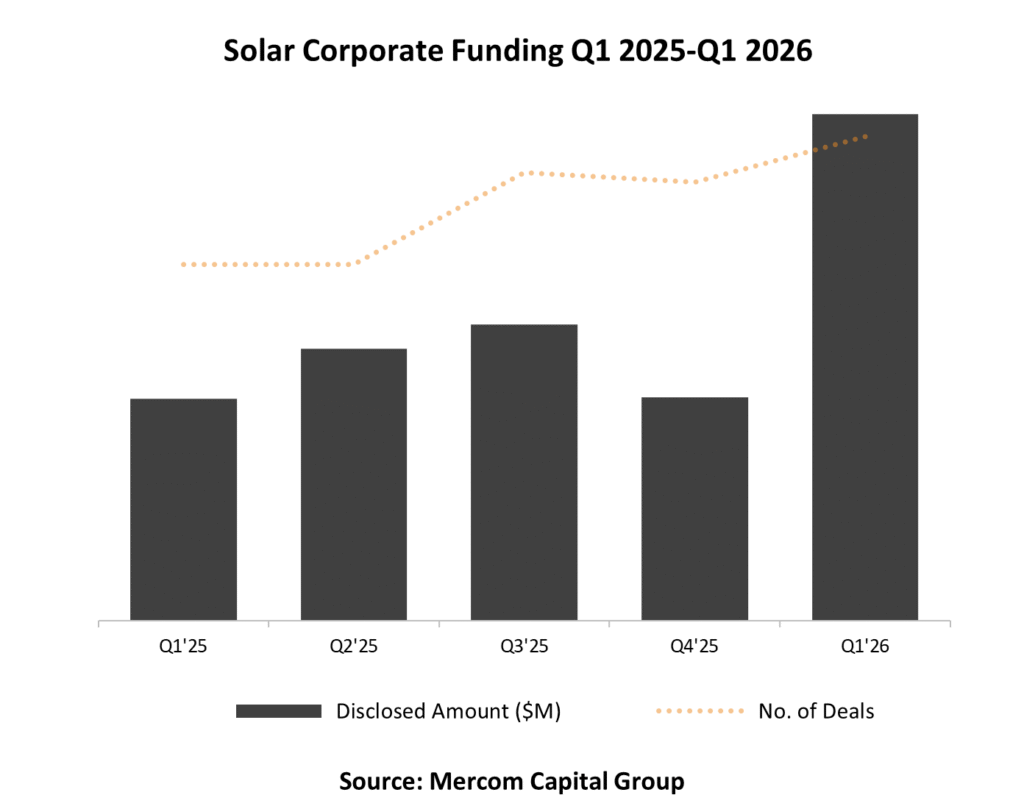

Total corporate funding in the solar sector reached $11.1 billion across 53 deals in Q1 2026, a 131% increase year-over-year (YoY) compared to $4.8 billion raised through 39 deals in Q1 2025. Funding was also up 127% quarter-over-quarter (QoQ) from the $4.9 billion raised in 48 deals in Q4 2025.

To learn more about Mercom’s Q1 2026 Annual Solar Funding and M&A Report, visit: https://mercomcapital.com/product/q1-2026-solar-funding-ma-report/

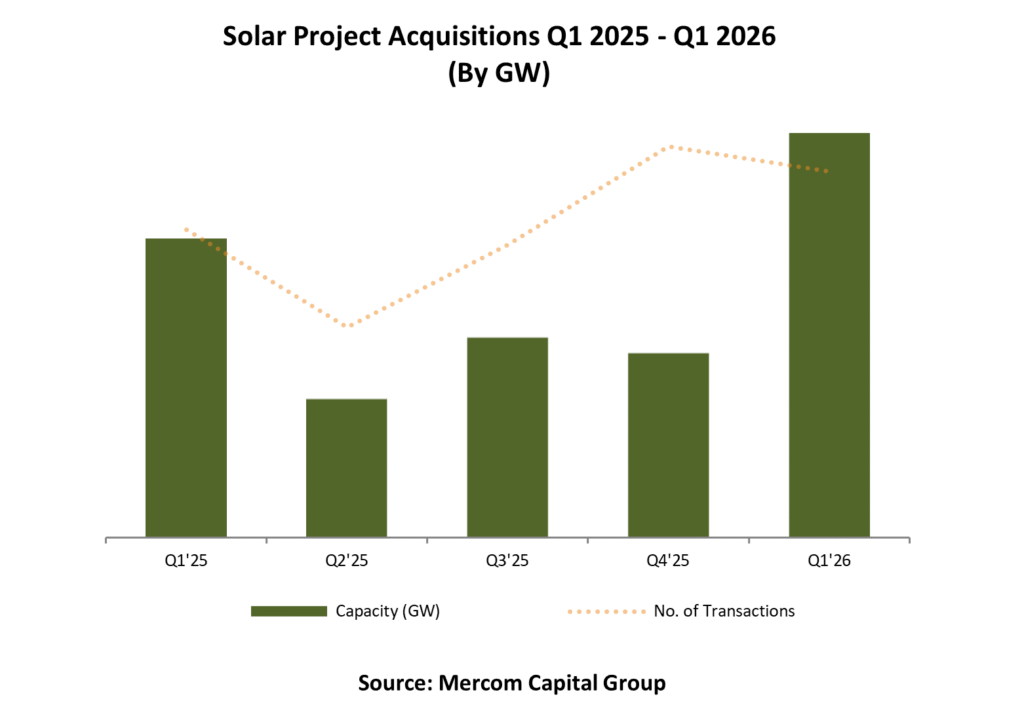

“Improved policy clarity and strong demand led to an increase in Solar funding and M&A activity in Q1 2026. Corporate funding was driven by larger transactions, particularly in debt financing, which reached its highest level in over a decade, while solar project acquisitions were at their highest capacity since 2022. Investments remained focused on assets that can advance in the near term, as projects moved forward following earlier policy and financing uncertainty, and developers accelerated timelines ahead of tax credit milestones. M&A activity continued to reflect demand for pipeline and scale across the sector,” said Raj Prabhu, CEO of Mercom Capital Group.

Global VC funding for the solar sector in Q1 2026 came to $1.1 billion in 17 deals, a 21% decrease YoY compared to $1.4 billion raised in 14 deals in Q1 2025. Funding increased 74% QoQ compared to the $606 million raised in 20 deals in Q4 2025.

The top VC/PE-funded companies in Q1 2026 were: Inox Clean Energy, which raised $343 million; Clean Max Enviro Energy Solutions with $165 million; Amarenco with $150 million; GREW Solar with $118 million; and Radiance Renewables with $100 million.

Of the $1.1 billion in VC funding raised across 17 deals during Q1 2026, 51% went to solar downstream companies, with $543 million in 10 deals. In Q4 2025, PV companies raised $423 million in four deals (70% of VC funding).

Public market financing in the solar sector totaled $1.1 billion across eight deals in Q1 2026, compared to $20 million raised in two deals in Q1 2025.

In Q1 2026, debt financing for the solar sector reached $8.9 billion across 28 deals, a 154% increase compared to the $3.5 billion secured in 23 deals in Q1 2025. On a QoQ basis, debt funding rose 162% from $3.4 billion across 20 deals in Q4 2025.

A total of 28 solar corporate M&A transactions were recorded in Q1 2026, a 47% increase compared to 19 transactions in Q1 2025, and up 33% compared to 21 solar M&A transactions in Q4 2025.

Solar downstream companies led corporate M&A activity with 19 transactions, followed by three acquisitions each in the Balance of System (BOS) and Equipment categories, two transactions by Manufacturers, and one transaction by a Service Provider.

Approximately 18.4 GW of solar projects changed hands in Q1 2026, up from 13.6 GW in Q1 2025. On a QoQ basis, project acquisition volume also increased, compared to 8.4 GW in Q4 2025.

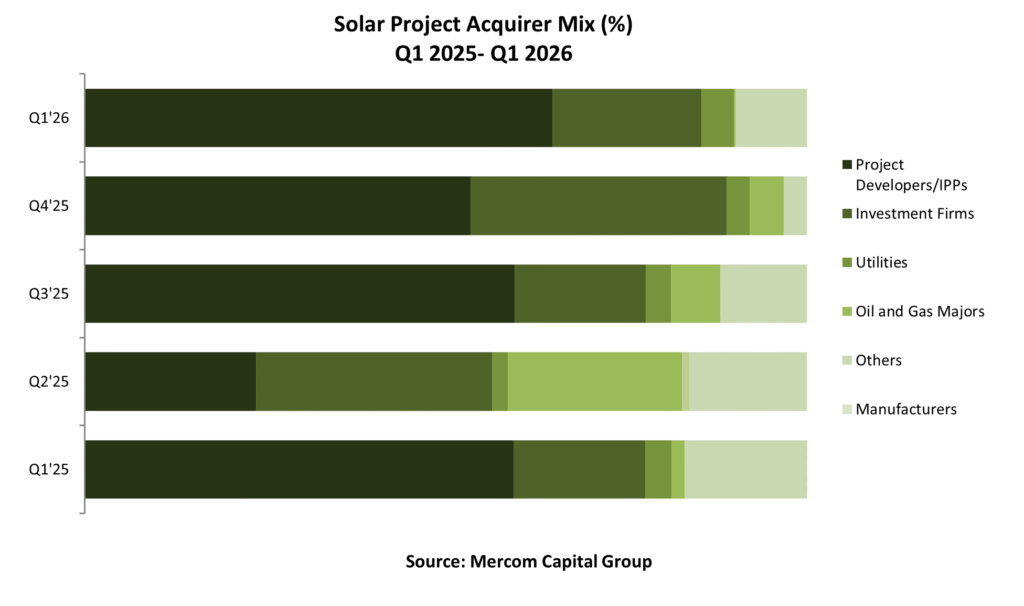

In Q1 2026, Project Developers and IPPs led solar project acquisitions, securing nearly 11.9 GW, followed by Investment Firms and Infrastructure Funds with 3.8 GW, and Other buyers (including energy companies, industrial conglomerates, engineering, and IT firms) with 1.8 GW. Additionally, a Utility company acquired an 830 MW project, an Oil and Gas firm acquired a 40 MW project, and a Manufacturing company acquired a 20 MW project.

In Q1 2026, Project Developers and IPPs led solar project acquisitions, securing nearly 11.9 GW, followed by Investment Firms and Infrastructure Funds with 3.8 GW, and Other buyers (including energy companies, industrial conglomerates, engineering, and IT firms) with 1.8 GW. Additionally, a Utility company acquired an 830 MW project, an Oil and Gas firm acquired a 40 MW project, and a Manufacturing company acquired a 20 MW project.

A total of 448 companies and investors are covered in this 62-page report, which contains 56 charts, graphs, and tables.

To learn more about Mercom’s Q1 2026 Annual Solar Funding and M&A Report, visit: https://mercomcapital.com/product/q1-2026-solar-funding-ma-report/