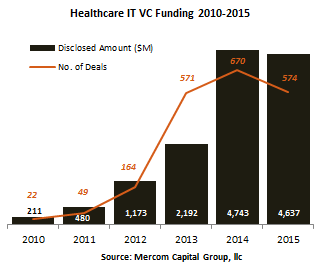

Venture capital (VC) funding, including private equity and corporate venture capital, in the Health IT sector totaled $4.6 billion in 574 deals in 2015, slightly below 2014’s record $4.7 billion in 670 deals – still a big year for the sector. Total corporate funding in Health IT companies including debt and public market financing (including IPOs) came to $7.9 billion this year, up slightly compared to $7.8 billion in 2014.

To learn more about the report, visit: https://mercom.wpengine.com/product/hit-201-funding-and-ma-report-all/

Since 2010, the sector has received $13.4 billion in VC funding in 2,050 deals and almost $7 billion in debt and public market financing (including IPOs), bringing the total funding for the sector to $20.4 billion.

“After an incredible run from 2010-2014, VC funding into Health IT companies leveled off last year. We are beginning to see a slow down in early stage deals, a sign the sector is beginning to mature. We are also seeing funding trends shift from practice-focused to consumer-focused technologies and products,” commented Raj Prabhu, CEO and Co-founder of Mercom Capital Group. “Apart from innovative technologies and solutions, business and revenue models are becoming more important.”

VC funding dipped in Q4 2015 with $1.1 billion in 145 deals compared to $1.6 billion in 148 deals in Q3 2015.

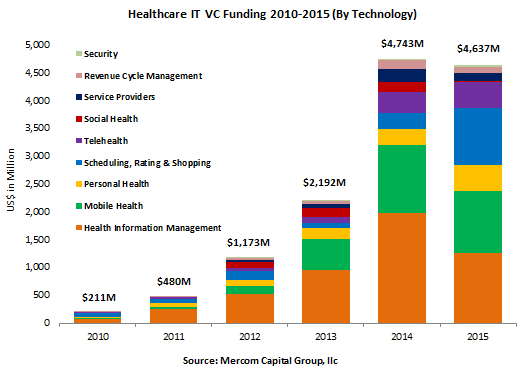

Practice-centric companies raised more than $1.5 billion in 171 deals in 2015, down from $2.4 billion in 234 deals last year. Top funded areas included – Data Analytics companies with $294 million, followed by Clinical Decision Support companies with $220 million and Practice Management Solutions companies with $183 million.

Consumer-centric companies grossed about $3.1 billion in 403 deals, up from $2.3 billion in 436 deals last year. Mobile Health (mHealth) companies raised the most funding with more than $1.1 billion. Most of the funding within the mHealth category went to mHealth Apps with $750 million and Wearables/Sensors with $277 million. Rating and Comparison Shopping companies received more than $1 billion followed by Telehealth companies with $468 million.

The areas with the highest YoY growth in funding were Comparison Shopping with 615 percent, Scheduling and Appointment Booking with 370 percent and Wellness with 126 percent.

Technology Areas with Highest Funding in 2015:

Scheduling/Appointment Booking: $790M

mHealth apps: $750M

Telemedicine: $439M

Wellness: $386M

Data Analytics: $294M

Wearables: $277M

Comparison Shopping: $232M

Top funded Health IT Technologies since 2010:

mHealth Apps: $1.4B

Scheduling/Appointment Booking: $1.1B

Wearables: $1B

Telemedicine: $929M

Clinical Decision Support: $899M

Data Analytics: $810M

Practice Management Solutions: $691M

Wellness: $671M

The top VC funding rounds in 2015 were Chinese company Guahao’s raise of $394 million, NantHealth’s $200 million round, ZocDoc’s $130 million raise, followed by Virgin Pulse’s $92 million raise. Practo was next with a $90 million round, Collective Health raised $81 million and Health Catalyst brought in $70 million.

A total of 909 investors participated in VC funding rounds for Healthcare IT companies in 2015 compared to 732 in 2014. The top VC investors in 2015 were New Enterprise Associates and Rock Health with nine deals each, followed by Merck Global Health Innovation Fund and Venrock with eight deals each.

There were 55 accelerator and incubator deals in 2015, a steep decline compared to 120 in 2014. Top accelerator/incubator investors were Sprint Accelerator, The Iron Yard, Relevant Health, Bayer Healthcare, DreamIt Health, Blueprint Health and New York eHealth Collaborative.

There were a total of 27 countries with Health IT VC funding deals in 2015.

There were 219 M&A transactions in the Health IT sector in 2015 compared to 220 transactions in 2014, with 27 companies making multiple transactions during the year.

“M&A deal activity was also flat year-over-year but, unlike funding, most of the companies acquired were practice focused as opposed to consumer focused,” continued Prabhu.

Mobile Health Apps had the most M&A transactions with 22, followed by Practice Management Solutions with 18 transactions, Data Analytics companies with 17, EHR/EMR companies with 16 and Telehealth companies with 11.

In the last five years, 166 companies have made multiple acquisitions including CompuGroup Medical and IMS Health with 10, Quality Systems with nine, Emdeon and iMedx with eight each, and PracticeMax with seven. GE Healthcare, McKesson, Roper Technologies, TELUS HEALTH and The Advisory Board Company each acquired six companies.

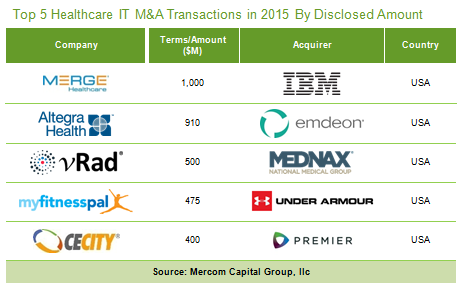

The Top 5 disclosed M&A transactions included the $1 billion acquisition of Merge Healthcare by IBM, the acquisition of Altegra Health by Emdeon for $910 million, the $500 million acquisition of Virtual Radiologic Corporation by MEDNAX, the $475 million acquisition of MyFitnessPal by Under Armour and the $400 million acquisition of CECity by Premier.

There were seven Digital Health IPOs this year, raising $2.2 billion. Fitbit raised $841.2 million, followed by Inovalon with $600 million, Press Ganey Associates with $256 million, Evolent Health with $225 million, Teladoc with $180 million, MINDBODY with $100.1 million and Adherium with $25.6 million.

There were seven Digital Health IPOs this year, raising $2.2 billion. Fitbit raised $841.2 million, followed by Inovalon with $600 million, Press Ganey Associates with $256 million, Evolent Health with $225 million, Teladoc with $180 million, MINDBODY with $100.1 million and Adherium with $25.6 million.

To learn more about the report, visit: https://mercom.wpengine.com/product/hit-201-funding-and-ma-report-all/