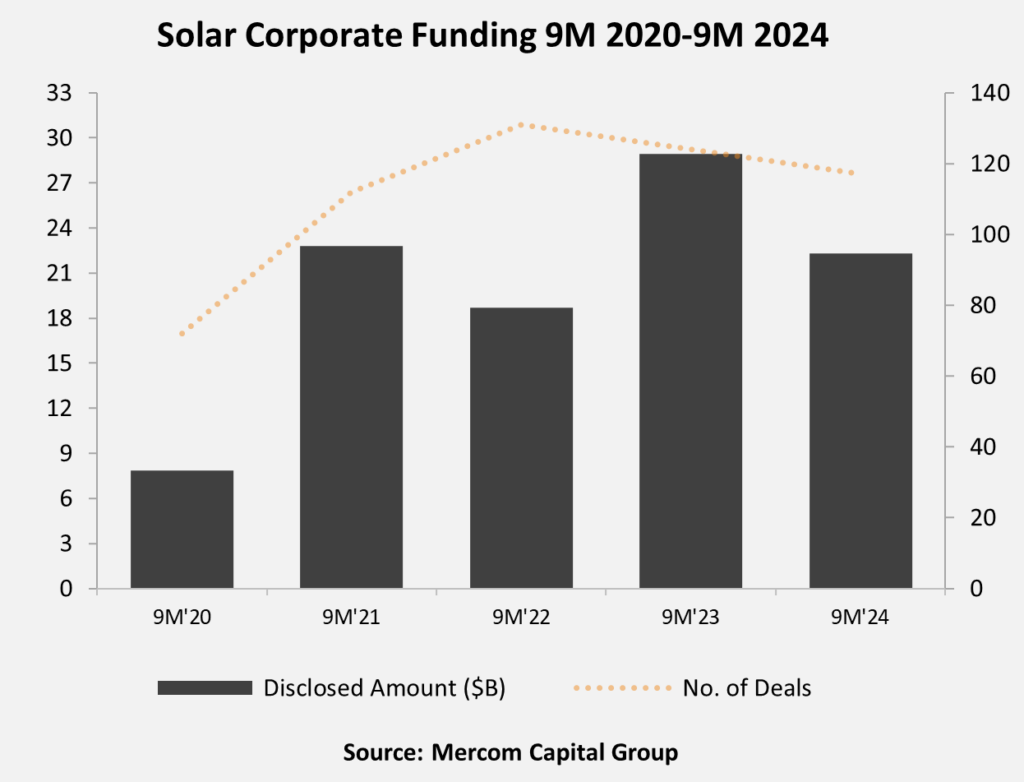

Total corporate funding, including venture capital (VC) funding, public market, and debt financing, in the first nine months (9M) of 2024 stood at $22.3 billion, 23% lower than the $28.9 billion raised in 9M 2023. The number of deals also decreased 6% year-over-year (YoY), with 117 deals in 9M 2024 compared to 124 deals during the same period last year.

“As we look at the financing activity in Q3 2024, it’s clear that the solar sector is grappling with significant uncertainties. Regulatory concerns around antidumping and countervailing duties and tariffs, the U.S. Section 45X guidance, potential policy shifts due to election outcomes, unpredictable global trade policies, supply chain disruptions, higher costs, tight labor markets, and ongoing project delays have all dampened investor confidence and delayed key investment decisions. While the recent 50 basis points rate cut is hopeful, the market needs more clarity and direction on future rate cuts to spark a resurgence in investment momentum,” said Raj Prabhu, CEO of Mercom Capital Group.

To get the report, visit: https://mercomcapital.com//product/9m-and-q3-2024-solar-funding-and-ma-report/

In 9M 2024, VC funding activity decreased 39% YoY, with $3.5 billion raised in 39 deals compared to the $5.7 billion raised in 51 deals in 9M 2023.

Solar downstream companies led financing activity with 32 deals worth $3.3 billion in 9M 2024.

The top VC deals in 9M 2024 were: $650 million raised by Pine Gate Renewables, $520 million raised by Nexamp, $440 million raised by BrightNight, $400 million raised by Doral Renewables, and $325 million raised by MN8 Energy.

Solar public market financing in 9M 2024 came to $2.1 billion in 10 deals, 71% lower YoY compared to $7.2 billion in 19 deals in 9M 2023.

Announced solar debt financing activity in 9M 2024 totaled $16.7 billion in 68 deals, 4% higher than 9M 2023, when $16 billion was raised in 54 deals.

In 9M 2024, 12 securitization deals totaled $3.8 billion, a 19% increase YoY compared to the $3.2 billion raised in 10 deals in 9M 2023.

In 9M 2024, 62 solar M&A transactions were executed compared to 75 in 9M 2023. The largest deal in the third quarter was by Macquarie Asset Management, which agreed to acquire a minority stake in D.E. Shaw Renewable Investments, a renewable energy project developer, through a number of its managed funds.

In 9M 2024, 166 project acquisitions totaling 28.3 GW were transacted compared to the same number of project acquisitions totaling 31.6 GW in 9M 2023.

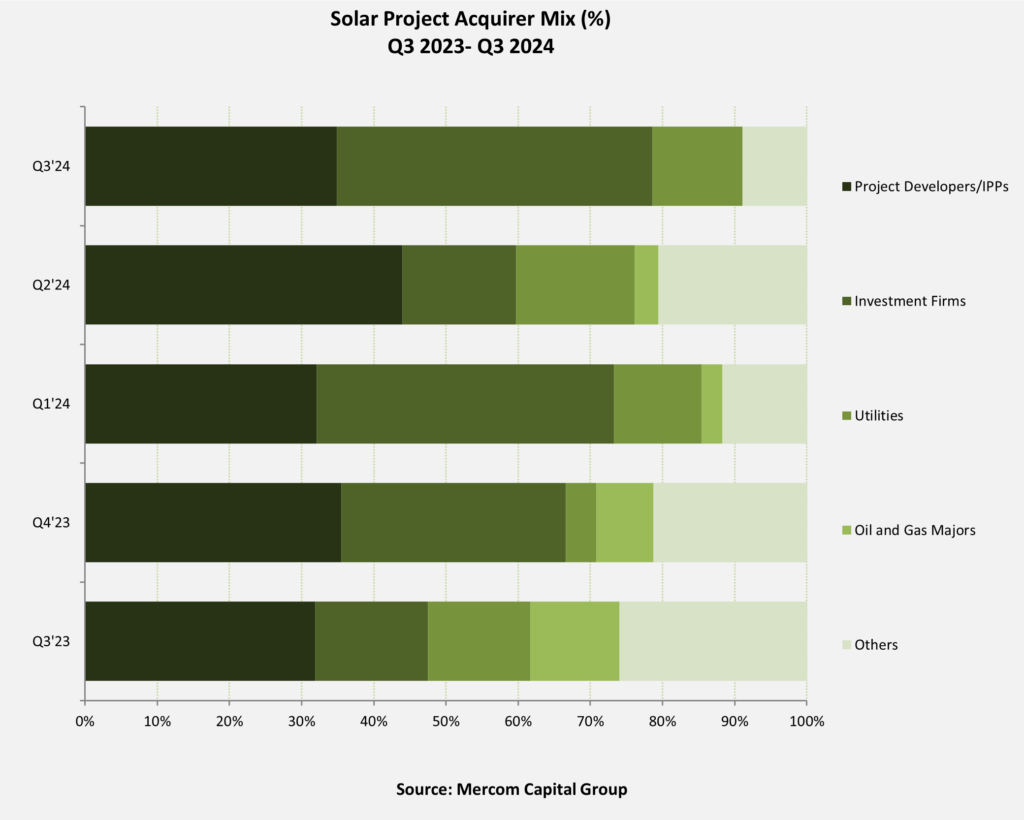

Investment firms were the most active acquirers of solar projects in Q3 2024, picking up 4.3 GW, followed by project developers and independent power producers (IPPs) with 3.4 GW. Utilities acquired 1.2 GW of solar projects, followed by 882 MW acquired by other companies (insurance providers, pension funds, energy trading companies, industrial conglomerates, and IT firms).

There are 247 companies and investors covered in this report. It is 95 pages long and contains 80 charts and tables.

To learn more about the report, visit:

https://mercomcapital.com//product/9m-and-q3-2024-solar-funding-and-ma-report/