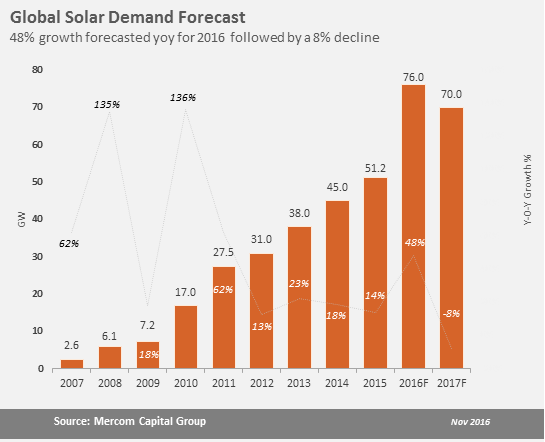

Mercom Capital Group, llc, a global clean energy communications and consulting firm, forecasts global solar installations to reach 76 GW in 2016. Solar installations to hit 70 GW in 2017.

Click here to get the full report: http://bit.ly/MercomSolarNov2016Form

“Global solar demand will overshoot most forecasts made earlier this year due to an unprecedented level of activity in China,” said Raj Prabhu, CEO and Co-Founder of Mercom Capital Group. “Record installations in China followed by a slowdown resulted in an oversupply situation, which led to a module price crash. Low module prices are helping demand recovery going into 2017.”

Rather than a slowdown as expected earlier, global solar demand outlook has improved for 2017 as steep module price declines have triggered a rebound in China in anticipation of the next round of tariff cuts. In fact, this latest rebound has stabilized module price declines somewhat. Similar demand recovery due to improved project economics is expected in other markets.

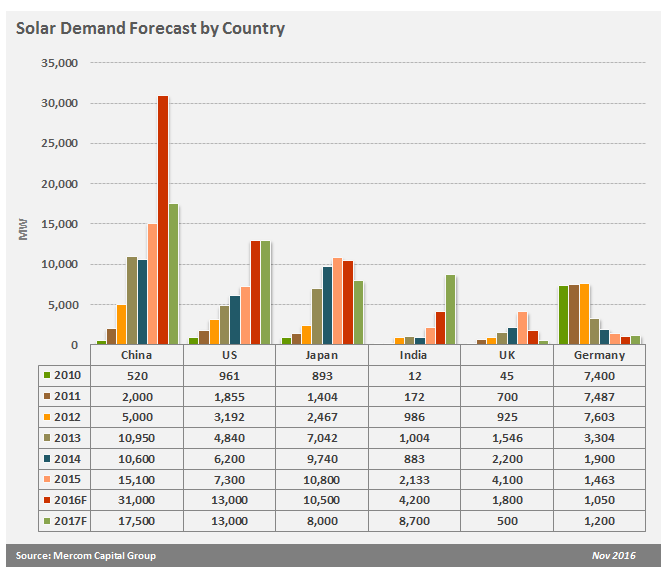

After installing 15.1 GW in 2015, China overshot its 2016 installation goal of 18.1 GW in the first half of 2016 alone with approximately 22 GW installed as developers rushed to complete projects before the country’s June 30 tariff deadline. Demand fell after the tariff cuts, which triggered a drop in solar module prices resulting in an oversupply situation. Spot module prices have fallen approximately 30 percent YTD and about 21 percent since June. Due to unprecedented installation levels, China’s National Energy Administration is looking at a 27 percent reduction in the country’s solar installation target from 150 GW to 110 GW by 2020.

Mercom’s forecast for the U.S. solar market in 2016 is approximately 13 GW. The forecast is mostly unchanged from our earlier estimates as channel checks have consistently indicated slower than expected activity after the ITC extension was announced in December 2015. A substantial number of large-scale projects have been postponed to 2017 due to the absence of an impending ITC deadline.

The U.S. market is projected to grow about 78 percent year-over-year in 2016. Utility-scale solar projects continue to drive the U.S. solar market with an estimated pipeline of more than 30 GW. Power purchase agreements (PPAs) are being signed at lower and lower prices and rapid module price declines due to the oversupply situation in China are expected to stimulate activity in the U.S. even more as project IRRs improve. All of this could lead to a strong 2017 for the U.S.

The unexpected election of Donald Trump has left the market questioning if it will be impacted by the results. While the U.S. Clean Power Plan, President Obama’s signature climate change policy, may be the first casualty, the ITC extension will likely remain due to the bipartisan nature of how the extension was passed and the fact that the solar sector employs more than 200,000 citizens.

Japan and India will follow China and the U.S. as the third and fourth largest markets this year. India has a chance to move up to the third spot in 2017 based on its current project pipeline. Japan is expected to install 10.5 GW this year. The tariff revisions coming up in Japan in April 2017 could be steep. Reverse auctions and regulations are also expected in April 2017 as Japan moves toward auctions in an effort to reduce subsidy bills. India is expected to install about 4 GW this year and double that in 2017. The Indian solar market is largely driven by auctions and has a robust 20 GW pipeline.

The European market continues to decline with only the U.K., Germany and France expected to install more than 1 GW in 2016. In 2017, France and Germany are the only European markets forecast to install more than a gigawatt.

Australia is expected to install approximately 1 GW in both 2016 and 2017.

Other solar markets to watch include Latin America, an important growth market led by Mexico, Chile and Brazil, and the Middle East and North Africa (MENA) region, which is also a significant up and coming market especially after the collapse of oil prices. South Africa and Saudi Arabia are forecast to show significant growth.

Subscribers to Mercom’s weekly Solar Market Intelligence Report will have access to the full update. To become a subscriber, visit: http://bit.ly/MercomSubscribe