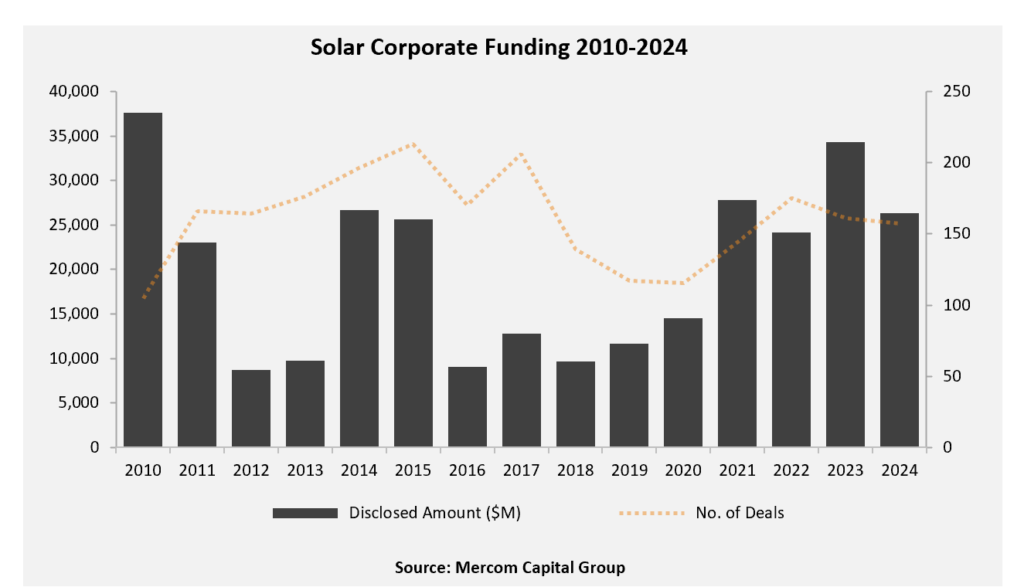

Total corporate funding, including venture capital (VC) funding, public market, and debt financing into the solar sector, decreased 24% year-over-year (YoY) in 2024, with $26.3 billion raised in 157 deals, compared to $34.4 billion in 161 deals in 2023.

“2024 was a year of uncertainties for the solar industry, with inflation, high interest rates, trade disputes, and policy ambiguity contributing to declines in funding and M&A activity. The market is awaiting clear policy signals from the new administration on the IRA provisions, ITC extensions, and tariff measures before investors come off the sidelines and deal-making can return to healthier levels,” commented Raj Prabhu, CEO of Mercom Capital Group.

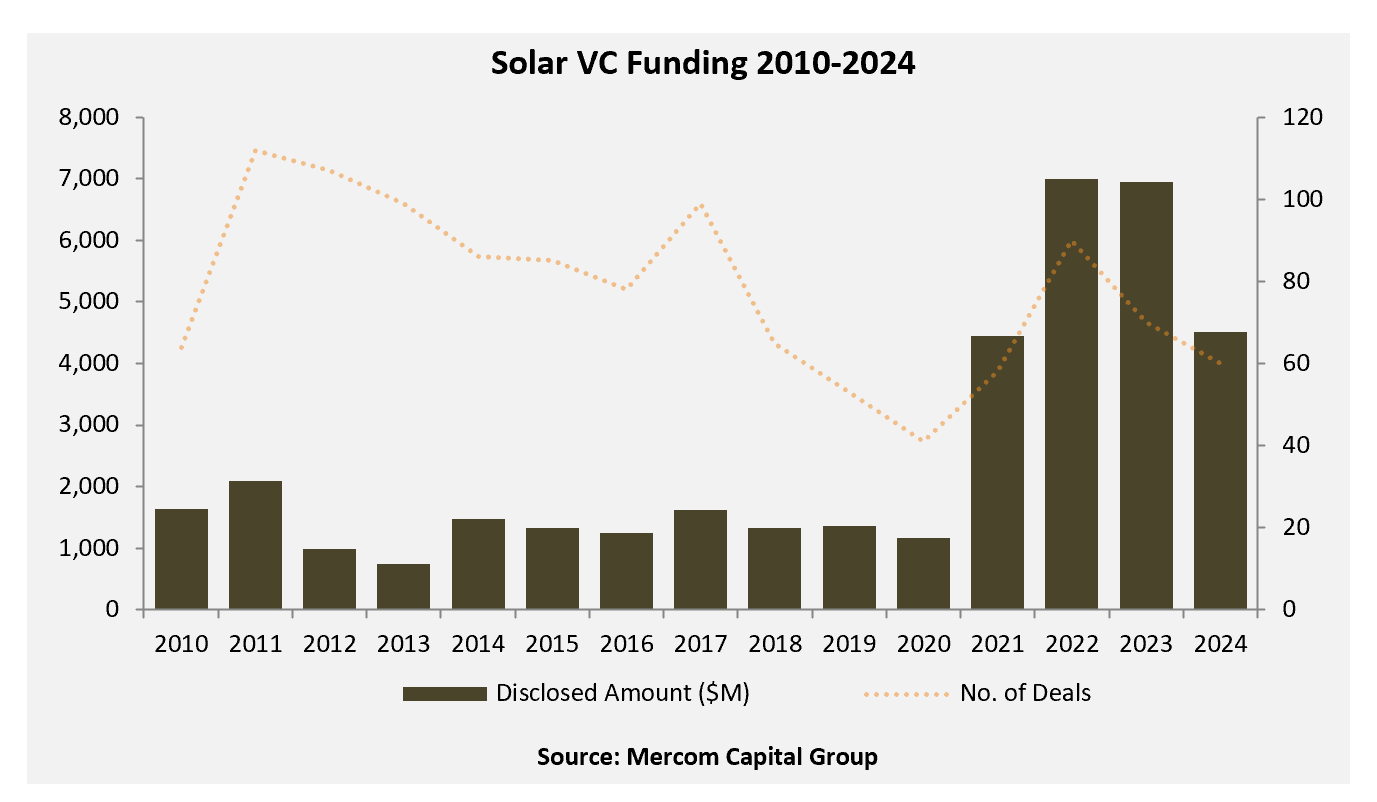

Global VC and private equity funding in the solar sector in 2024 came to $4.5 billion in 60 deals, 36% lower than the $7 billion raised in 70 deals in 2023. There were 14 VC funding deals of $100 million or more in 2024.

Of the $4.5 billion in VC funding raised in 60 deals in 2024, $3.9 billion (87%) went to Solar Downstream companies. Solar PV companies raised $401 million; Thin film companies raised $33 million; and Service Providers raised $1 million.

The top VC-funded companies in 2024 were Pine Gate Renewables ($650 million), Nexamp ($520 million), BrightNight ($440 million), Doral Renewables ($400 million) and MN8 Energy ($325 million).

Public market financing in the solar sector in 2024 totaled $3 billion, 59% lower than the $7.4 billion raised in 2023. Nine companies went public in 2024, bringing in $1.3 billion, compared to seven companies that raised $2.1 billion in 2023.

In 2024, announced debt financing came to $18.8 billion, 6% lower compared to $20 billion in 2023. Securitization deals were a key contributor, with a record $5 billion in 16 deals.

M&A activity was 15% lower YoY in 2024, with 82 corporate M&A transactions compared to 96 in 2023. The largest transaction was by Brookfield Asset Management, along with institutional partners, including Brookfield Renewable and Singapore’s Temasek Holdings, which agreed to acquire a 53.12% stake in Neoen, a solar, wind, and energy storage project developer, for $6.54 billion.

Solar Downstream companies led corporate M&A activity in 2024, acquiring 66 companies, followed by Manufacturers with six, and Service Providers and Balance of System (BOS) companies with five acquisitions each.

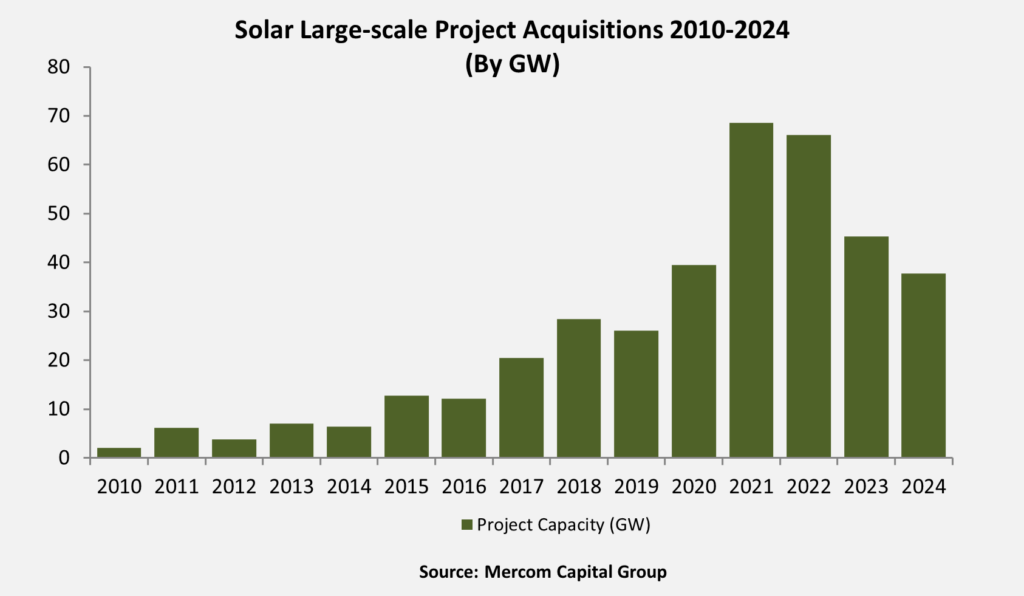

The number of large-scale solar project acquisitions in 2024 fell to 217, compared to 231 in 2023. The total acquired capacity also dropped to 37.7 GW, a 17% decrease from 45.4 GW the previous year.

Of the 37.7 GW of large-scale solar projects acquired in 2024, 38% were acquired by Project Developers and IPPs. Investment Firms and Infrastructure Funds acquired 35%, followed by Others (insurance providers, pension funds, energy trading companies, industrial conglomerates, and IT firms), with 13% in 2024. Utilities, Oil and Gas, and Installers acquired the remaining 14%.

Two hundred and eighty-nine (289) companies and investors are covered in this 136-page report, which contains 107 charts, graphs, and tables.

To learn more about Mercom’s 2024 Annual Solar Funding and M&A Report, visit: https://mercomcapital.com/product/annual-and-q4-2024-solar-funding-and-ma-report